Hailstorms don’t knock first. They hit hard, move fast, and leave behind damage that isn’t always obvious but almost always costly. If you’re dealing with a roof hail damage insurance claim Texas, understanding what actually matters can make the difference between a partial payout and full recovery. And in storm-prone areas like Irving, that difference shows up quickly on your roof and in your finances.

Here’s the reality: insurance claims are not just about damage. They’re about proof, timing, and leverage. Miss one piece, and your claim weakens. Get all three right, and you take control. Let’s break it down.

Understanding Hail Damage: What Actually Happens to Your Roof

Hail damage is deceptive. It rarely looks catastrophic right away. No dramatic holes. No immediate flooding. Just small, scattered impacts that quietly compromise your roof.

That’s what makes it dangerous. When hailstones strike, they compress materials. They fracture protective layers. They loosen seals. These micro-damages spread over time, leading to leaks, insulation failure, and even structural issues.

Key Factors That Influence Damage

- Density over size

A dense hailstone can cause more damage than a larger, softer one. - Wind velocity

Wind-driven hail hits harder and at angles. - Material composition

Asphalt absorbs impact. Metal dents. Tile fractures. - Aging roofs

Older roofs are more vulnerable to damage.

Insurance companies evaluate functional damage. That means anything that affects your roof’s ability to protect your home critical when filing a hail roof damage insurance claim.

How to Identify Hail Damage by Roof Type (Advanced Breakdown)

Not all roofs respond the same way. Identifying the right type of damage is key to building a strong hail damage on roof insurance claim.

Asphalt Shingle Roofs

Look for:

- Granule loss exposing dark spots

- Soft bruising beneath the surface

- Random impact patterns

- Circular or irregular marks

Granule loss is a major red flag. It reduces the lifespan of your roof significantly.

Metal Roofs

Watch for:

- Dents and dimples

- Seam and fastener damage

- Scratches exposing metal

Many insurers call this cosmetic. But coating damage leads to corrosion making it functional.

Tile Roofs (Clay or Concrete)

Check for:

- Cracks or fractures

- Dislodged tiles

- Hidden subsurface damage

Even a single cracked tile can lead to leaks.

Flat and Low-Slope Roofs

Look for:

- Membrane punctures

- Bubbling or blistering

- Drainage changes

Damage here often develops slowly, making early documentation essential.

Immediate Steps to Take After a Hailstorm

What you do next shapes your entire claim.

Action Plan

- Stay safe avoid climbing immediately

- Take photos from the ground

- Inspect gutters and siding

- Record storm details

- Prevent further damage

- Contact your insurer

In Irving, where hailstorms can impact entire neighborhoods, acting quickly helps you stay ahead of delays.

How to Document Hail Damage for Your Insurance Claim

If you’re serious about getting paid fairly, mastering How to Document Hail Damage for an Insurance Claim is essential. Documentation is what turns damage into dollars.

What to Photograph

- Roof (wide and close-up views)

- Impact points

- Gutters, vents, flashing

- Interior ceilings

What to Record

- Storm date and time

- Weather reports

- Damage timeline

Documentation Table

| Type | Purpose | Tip |

| Photos | Proof | Capture multiple angles |

| Video | Context | Walk around slowly |

| Notes | Timeline | Record immediately |

| Reports | Credibility | Use professional inspections |

Advanced Insight

Supplements rely on detailed estimating software like Xactimate. Precision matters. In fact, the level of detail required can be compared to concepts like the Fourier transform, where even small variations can significantly impact results. The same applies to your claim small missed details can mean big financial differences.

What Insurance Carriers Commonly Miss in Their Scope

This is where many claims fall short and why understanding Hail Damage Claim Supplements: What Carriers Miss in Their Scope gives you a major advantage.

Commonly Missed Items

- Ridge caps

- Flashing

- Underlayment

- Vent covers

Interior Damage

Water intrusion often appears later and is frequently excluded.

Pricing Gaps

- Outdated material costs

- Missing labor details

- Incomplete scope items

A partial estimate leads to a partial payout. That’s why reviewing your hail roof damage insurance claim carefully is critical.

The Supplement Process: Getting Paid What You’re Owed

Supplements close the gap between initial estimates and real repair costs.

What Is a Supplement?

An updated claim request for additional damage or costs.

When It’s Needed

- Hidden damage

- Code upgrades

- Material mismatches

Process Overview

- Identify additional damage

- Submit documentation

- Carrier reviews

- Payment adjusted

Mistakes to Avoid

- Accepting the first offer

- Starting repairs early

- Weak documentation

A strong supplement can significantly increase your roof hail damage insurance claim Texas payout.

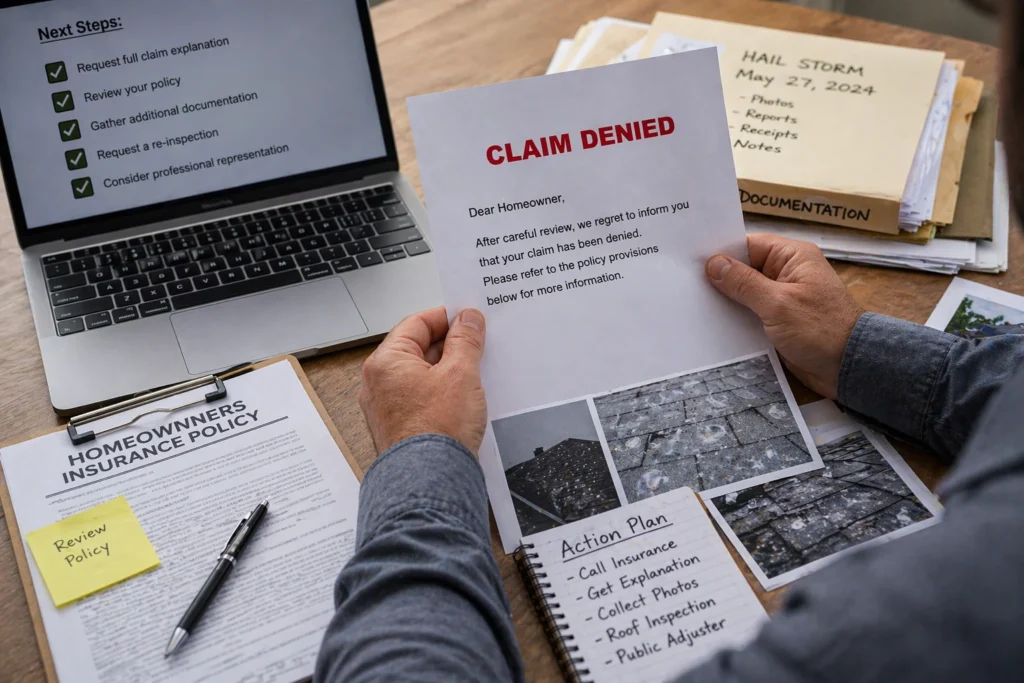

What to Do If Your Hail Claim Was Denied in Texas

A denial isn’t the end it’s often the beginning of a stronger claim.

If you’re dealing with What to Do If Your Hail Claim Was Denied in Texas, here’s what matters:

- Request a full claim explanation

- Review your policy carefully

- Gather additional documentation

- Request a re-inspection

- Consider professional representation

Many denied claims are overturned with stronger evidence and proper negotiation.

Why Hiring a Public Adjuster Changes the Outcome

Understanding Public Adjuster vs. Insurance Adjuster for Hail Claims in Texas is critical.

Key Difference

- Insurance adjuster works for the carrier

- Public adjuster works for you

What a Public Adjuster Does

- Inspects thoroughly

- Documents all damage

- Negotiates directly

- Maximizes claim value

Why It Matters

Insurance companies handle thousands of claims. You get one chance to get it right. In Irving, where hail events are frequent, having professional representation often leads to stronger outcomes.

Common Mistakes That Cost Homeowners Thousands

Avoid these:

- Waiting too long

- Assuming no visible damage

- Accepting first estimates

- Poor documentation

- Hiring inexperienced contractors

Each one reduces your claim value.

Real-World Scenario: Two Homeowners, Two Outcomes

Same storm. Same neighborhood.

Homeowner A

- Filed quickly

- Documented thoroughly

- Used professional help

Outcome: Full replacement approved

Homeowner B

- Waited

- Minimal documentation

- Accepted initial offer

Outcome: Partial payout

The difference? Strategy.

How to Protect Your Roof Before the Next Storm

Preparation changes everything.

Preventive Steps

- Annual inspections

- Impact-resistant shingles

- Proper drainage maintenance

- Tree trimming

Upgrade Table

| Upgrade | Benefit | Long-Term Value |

| Impact shingles | Less damage | Fewer repairs |

| Metal upgrades | Durability | Longevity |

| Inspections | Early detection | Cost savings |

Why This Matters More in Irving

Irving homeowners face repeated hail exposure.

That means:

- More claims

- More scrutiny

- Greater risk of underpayment

Understanding how to manage a roof hail damage insurance claim Texas puts you ahead.

Final Takeaway: Control the Claim Before It Controls You

Hailstorms are unpredictable. Your response isn’t. When you understand damage, document properly, and manage your claim strategically, everything changes. Act early. Stay organized. Don’t settle. Because protecting your roof isn’t just about repairs it’s about protecting your home, your finances, and your peace of mind.

FAQs

Look for signs like granule loss, dents, cracks, or soft spots depending on your roof type.

Yes, many types of hail damage are subtle and worsen over time if not addressed.

You should file as soon as possible after the storm to avoid delays or disputes.

Most policies cover functional damage that affects the roof’s ability to protect your home.

You can do a basic visual check, but professional inspections are safer and more accurate.

It’s an additional request for payment when more damage is found after the initial estimate.

Claims are often denied due to insufficient evidence, late filing, or disputes over damage type.

A public adjuster can help document damage and negotiate for a higher, more accurate payout.

Usually no coverage is typically limited to functional damage that impacts performance.

Waiting too long and failing to document the damage properly.