Hail storms don’t just dent roofs they create gaps in insurance estimates. And those gaps? They cost homeowners thousands. That’s exactly where hail damage claim supplements: what carriers miss in their scope becomes critical. If you’ve ever looked at an insurance estimate and felt it didn’t fully capture the damage, you’re not alone. Most initial scopes are incomplete.

I’ve seen it too many times. The estimate looks polished. Organized. Official. But once you break it down line by line, the holes appear. Missing components. Underpriced labor. Ignored code requirements. This is where hail damage claim supplements: what carriers miss in their scope turns a basic payout into a fully justified claim especially when backed by expert use of Xactimate. Let’s dig in. No filler. Just actionable, real-world insight.

Understanding Hail Damage Beyond the Surface

Hail damage is deceptive. It rarely announces itself loudly. From the street, your roof might look perfectly intact. No obvious destruction. No missing sections. But that doesn’t mean it’s undamaged. In fact, most hail damage hides in plain sight.

Here’s what’s really happening:

- Granule loss reduces UV protection

- Bruising weakens shingle integrity

- Micro-fractures shorten lifespan dramatically

Different materials react in different ways:

- Asphalt shingles: Soft impacts that break internal structure

- Metal roofing: Dents that compromise coatings and lead to corrosion

- Tile roofing: Hairline cracks that spread over time

Quick inspections don’t catch these details. And when details are missed, estimates fall short. That’s the starting point for hail damage claim supplements: what carriers miss in their scope.

What Is a Hail Damage Claim Supplement?

A supplement is not a redo. It’s a correction. A hail damage claim supplement is an additional request for compensation based on damage that was overlooked, underestimated, or discovered after the initial inspection.

Think of it like this:

- Initial claim = first draft

- Supplement = final, accurate version

And here’s the truth: most claims need one.

Why? Because initial inspections are often rushed. Adjusters are juggling dozens of claims after a storm. They’re under pressure. They move fast. And fast means incomplete. That’s why hail damage claim supplements: what carriers miss in their scope exists to close that gap.

Why Insurance Carriers Miss Critical Damage

Let’s be fair but honest. Insurance carriers don’t always intentionally miss items. But the system they operate in makes it likely.

Key Reasons for Missed Scope Items

- High claim volume: After storms, adjusters are overloaded

- Time constraints: Limited time per inspection

- Cost containment: Lower estimates protect company margins

- Surface-level evaluations: No deep dive into materials

You’ll often see familiar phrases:

- “Damage is cosmetic only”

- “Repair is sufficient”

- “No functional damage observed”

These phrases can feel final. But they’re not. They’re entry points into hail damage claim supplements: what carriers miss in their scope.

The Most Common Items Missing from Insurance Scopes

This is where homeowners lose money quietly.

Roofing Components Frequently Overlooked

- Starter shingles

- Ridge caps

- Drip edge

- Underlayment

- Ice & water shield

Exterior Elements Often Ignored

- Gutters and downspouts

- Window screens

- Siding dents

- Garage doors

Interior Damage

- Ceiling stains

- Wet insulation

- Drywall bubbling

Code Compliance Upgrades

Building codes change. Roofs must meet current standards not old ones. But many estimates skip these upgrades entirely.

Here’s a clearer breakdown:

| Category | Missed Item | Impact |

| Roofing | Underlayment | Required for full system integrity |

| Exterior | Gutters | Essential drainage system |

| Interior | Insulation | Hidden moisture damage |

| Code | Ventilation | Required for compliance |

Miss these? You’re covering the cost yourself.

The Power of Xactimate in Supplementing Claims

This is where expertise separates outcomes. Xactimate is the industry standard. It’s what insurance companies use. But here’s the reality not all Xactimate estimates are created equal.

A basic estimate might include:

- Limited line items

- Simplified labor

- Minimal detail

A detailed estimate includes:

- Exact measurements

- Full component breakdown

- Labor, waste, overhead, and profit

- Local pricing updates

Hail damage claim supplements: what carriers miss in their scope becomes far easier to prove when your supplement matches the carrier’s system but exceeds it in accuracy.

How Xactimate Expertise Changes the Outcome

This isn’t just about software. It’s about how you use it.

A well-built supplement:

- Speaks the carrier’s language

- Includes precise line items

- Justifies every addition

- Anticipates objections

Here’s a comparison:

| Estimate Type | Detail Level | Approval Likelihood |

| Basic Scope | Low | Moderate |

| Expert Xactimate | High | High |

The difference isn’t small. It’s massive.

Step-by-Step: How the Supplement Process Works

Let’s make it simple and practical.

1. Review the Initial Estimate

Read every line. Look for what’s missing—not just what’s included.

2. Conduct a Detailed Re-Inspection

Take photos. Document everything. Don’t rush.

3. Compare Against Contractor Findings

This is where discrepancies show up.

4. Build a Full Xactimate Estimate

Include every necessary component.

5. Submit the Supplement

Attach documentation and justification.

6. Negotiate

Expect pushback. Stay consistent.

7. Secure Approval

Adjustments are made. Payment increases.

That’s hail damage claim supplements: what carriers miss in their scope in motion.

Documentation: The Backbone of a Strong Supplement

No documentation, no leverage. It’s that simple.

What Strong Documentation Looks Like

- High-resolution photos (close + wide)

- Measurement reports

- Material specifications

- Contractor estimates

Weak documentation leads to delays. Or worse denials.

Strong documentation forces clarity.

Advanced Documentation Tips That Make a Difference

Want to take it further? Here’s what professionals do:

- Photograph in sequence to show progression

- Use chalk to highlight hail hits

- Add timestamps for credibility

- Capture collateral damage (AC units, vents, siding)

Small details create big results.

Deep Dive: Xactimate Line Items That Change Everything

This is where most supplements either win or fall apart.

Xactimate isn’t just a tool. It’s a language. And if you don’t speak it fluently, your supplement gets ignored or reduced.

Critical Line Items Often Missed

- Tear-off and disposal fees

- Drip edge replacement (per linear foot)

- Starter strip installation

- Ridge cap shingles

- Flashing replacement around penetrations

- Valley metal installation

- Ice & water barrier

- Ventilation upgrades

Why Line Items Matter

Carriers don’t approve vague requests. They approve structured, itemized scopes.

Compare this:

- “Roof repair needed”

- “Remove 25 SQ laminate shingles, replace with starter, ridge cap, drip edge, and underlayment per code”

Precision wins. Every time.

Contractor Estimate vs. Insurance Scope: The Hidden Gap

This is one of the biggest friction points.

Contractors often provide:

- Lump-sum estimates

- Broad repair descriptions

Insurance carriers expect:

- Itemized Xactimate line items

- Specific measurements

- Justification notes

Example Comparison

| Category | Contractor Estimate | Insurance Scope |

| Roof | $15,000 total | $9,200 itemized |

| Gutters | Included | Excluded |

| Flashing | Included | Not listed |

This gap is exactly why hail damage claim supplements: what carriers miss in their scope exists.

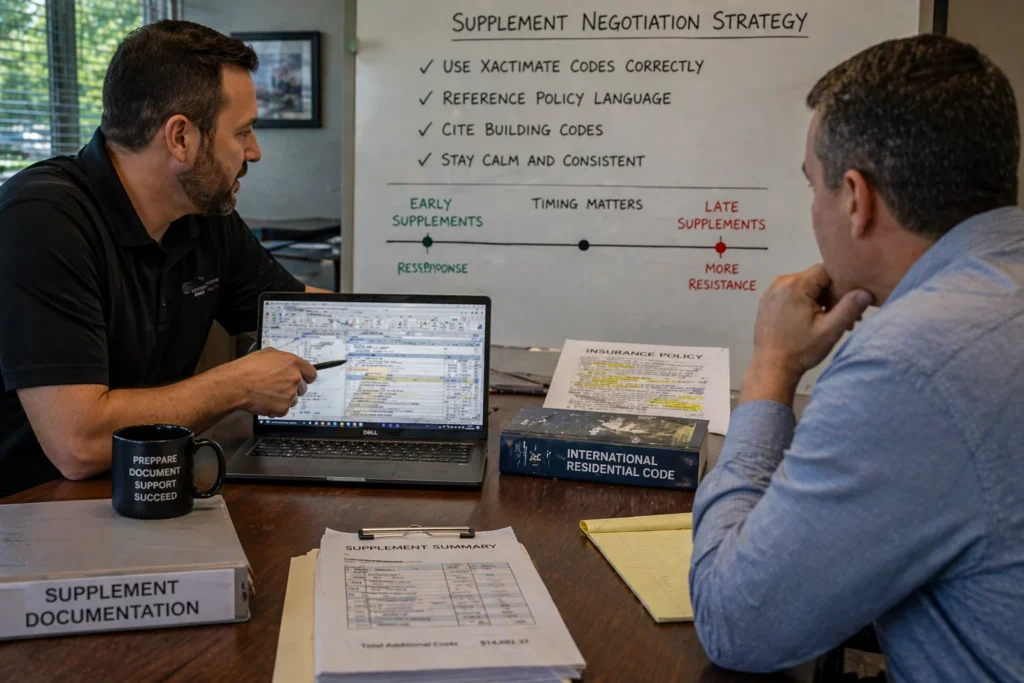

Building Leverage in Supplement Negotiations

Negotiation isn’t about pressure. It’s about precision.

Effective Strategies

- Use Xactimate codes correctly

- Reference policy language

- Cite building codes

- Stay calm and consistent

Timing matters too. Early supplements move faster. Late ones face more resistance.

The Financial Impact of Missed Scope Items

Let’s talk numbers.

| Scope Type | Initial Estimate | After Supplement |

| Roof Only | $9,500 | $16,200 |

| Full Exterior | $14,000 | $25,800 |

That gap? That’s what hail damage claim supplements: what carriers miss in their scope recovers.

Without it, homeowners pay out of pocket.

Why Homeowners in Irving Are Especially Affected

Storm activity in Irving creates a perfect scenario for under-scoped claims.

Here’s why:

- Frequent hail events

- High claim volume

- Aging roofing systems

- Updated building codes

Homes in Irving often require more detailed scopes than what initial inspections provide.

Local Insight

Many homes in Irving were built during rapid development phases. That means:

- Older materials still in use

- Multiple roof layers in some cases

- Code upgrades not reflected in initial builds

This increases supplement opportunities and risks if ignored. Local expertise matters. A lot.

DIY vs. Professional Supplementing

You can do it yourself. But should you?

DIY Risks

- Missing line items

- Incorrect pricing

- Weak documentation

- Accepting low offers

Professional Advantages

- Deep Xactimate expertise

- Strong negotiation skills

- Faster approvals

- Higher payouts

This isn’t just paperwork. It’s strategy.

When to Request a Supplement

Timing is everything.

Request a Supplement When:

- Your estimate feels low

- Contractor quotes are higher

- Damage was missed

- Repairs reveal additional issues

If something doesn’t add up, it probably doesn’t.

If your claim has already been denied, understanding What to Do If Your Hail Claim Was Denied in Texas becomes a critical next step before pursuing additional action.

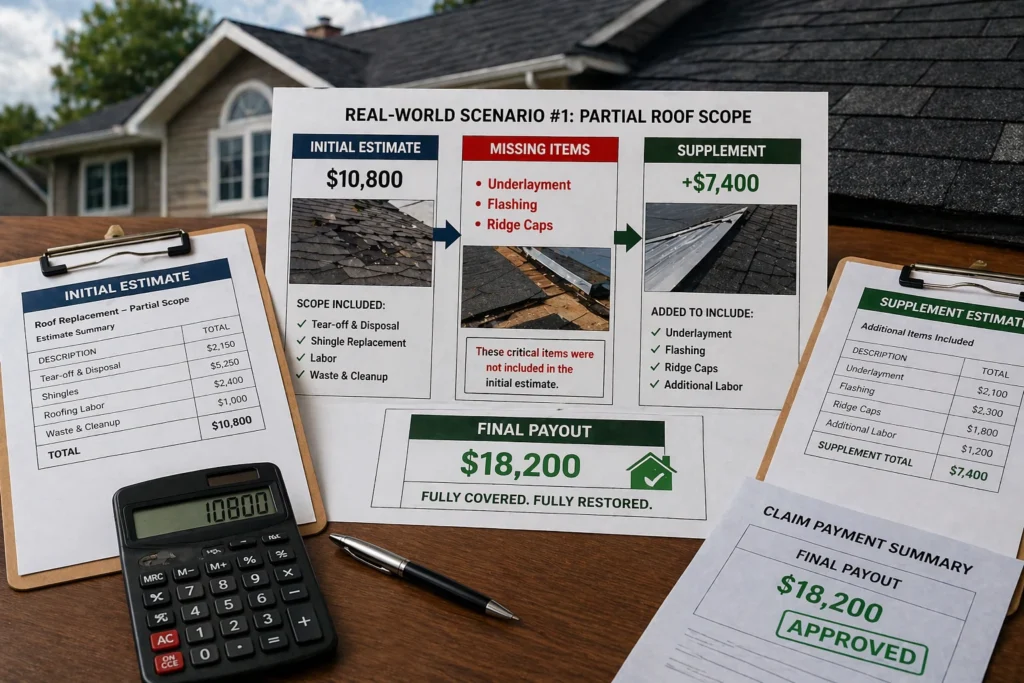

Real-World Scenario #1: Partial Roof Scope

- Initial estimate: $10,800

- Missing: underlayment, flashing, ridge caps

- Supplement: +$7,400

- Final payout: $18,200

Real-World Scenario #2: Full Exterior Recovery

- Initial estimate: $13,600

- Missing: gutters, siding, window screens

- Supplement: +$11,300

- Final payout: $24,900

These aren’t rare outcomes. They’re common.

That’s the power of hail damage claim supplements: what carriers miss in their scope.

Advanced Insight: Why Detail Changes Everything

In complex systems, small details drive outcomes. This is similar to entropy in physics, where disorder increases without structure. In your claim, every photo, measurement, and line item adds structure and clarity. More detail = stronger position.

Common Mistakes That Kill Supplements

Avoid these at all costs:

- Submitting vague estimates

- Using incorrect pricing

- Skipping documentation

- Accepting first responses as final

Each mistake weakens your leverage.

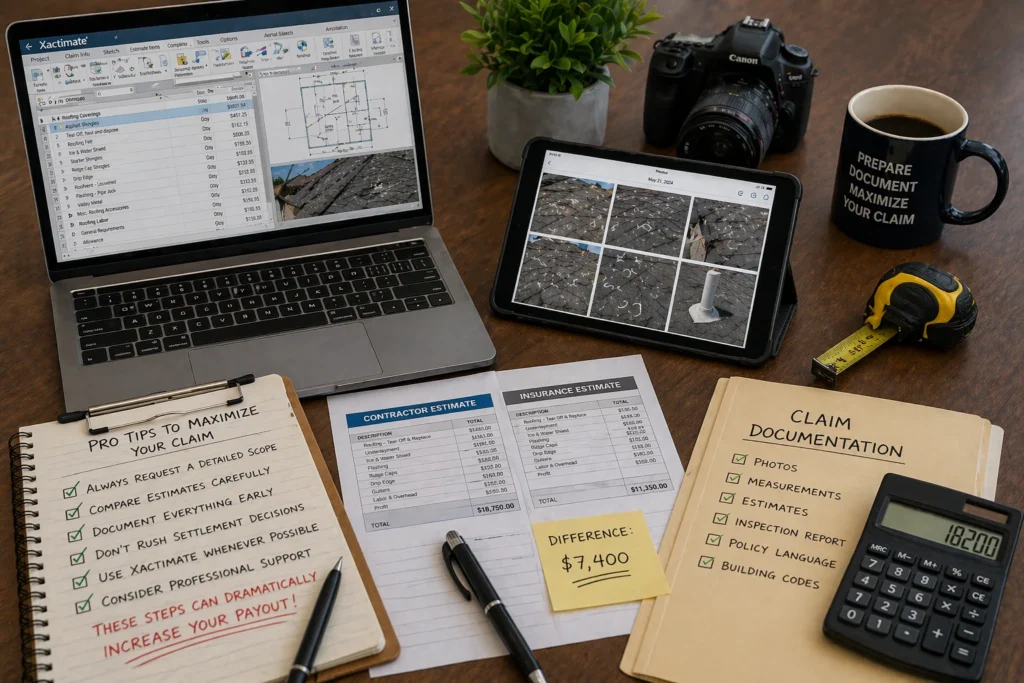

Pro Tips to Maximize Your Claim

- Always request a detailed scope

- Compare estimates carefully

- Document everything early

- Don’t rush settlement decisions

- Use Xactimate whenever possible

- Consider professional support

These steps alone can dramatically increase your payout.

Final Thoughts: Don’t Leave Money on the Table

Here’s the reality. Insurance estimates are starting points. Not final answers. If something feels incomplete, trust that instinct. Investigate it. Challenge it. Fix it. Hail damage claim supplements: what carriers miss in their scope is about accuracy, fairness, and full recovery. Nothing more. Nothing less.

For homeowners in Irving, this process isn’t optional it’s essential. Storms will keep coming. Claims will keep happening. But with the right approach and strong Xactimate expertise you stay in control. And that’s how you turn a partial payout into a complete one.

FAQs

A supplement is an additional request for funds to cover damage missed or underestimated in the original insurance estimate.

High claim volume, time constraints, and surface-level inspections often lead to incomplete scopes.

If your contractor’s estimate is higher or you notice missing items, a supplement is likely needed.

Xactimate provides detailed, standardized estimates that align with insurance carrier expectations.

Yes, but without proper documentation and Xactimate knowledge, approval can be more difficult.

Underlayment, flashing, gutters, and code-required upgrades are frequently overlooked.

It can take a few days to several weeks, depending on documentation and carrier response time.

It may extend the timeline slightly, but it often results in a significantly higher payout.

You can still reopen the claim or submit additional evidence to support a reconsideration.

Not always, but strong documentation and accurate scoping greatly increase the chances.