Getting a denial letter after a storm hits hard. It feels final. It feels like the end of the road. It’s not. If you’re searching for What to Do If Your Hail Claim Was Denied in Texas, you’re already doing something most homeowners don’t you’re pushing back. And that matters more than you think.

Hail damage claims are denied more often than people expect across Texas. In cities like Irving, where storms can roll through fast and claims stack up quickly, insurance companies often process inspections under pressure. That means mistakes happen. Damage gets missed. Claims get undervalued or denied outright.

Here’s the reality: a denial is not a verdict. It’s a position. And positions can be challenged. This guide gives you a clear, strategic roadmap. Not just what to do but how to do it effectively so you actually improve your chances of getting paid.

Why Hail Claims Get Denied in Texas

Before you fight back, understand what you’re up against.

Common Reasons for Denial

Insurance companies typically rely on a handful of explanations:

- “No storm-related damage found”

- Damage classified as wear and tear

- Missed filing deadlines

- Lack of documentation

- Policy exclusions

At first glance, these reasons seem firm. But they’re often based on limited information.

Insurance Company Limitations (and Realities)

Adjusters are human. They work fast. And after a major storm, they may inspect dozens of homes in a single day.

That creates problems:

- Inspections can be rushed

- Subtle damage gets overlooked

- Reports rely on generalized assumptions

Interestingly, this kind of decision-making under uncertainty mirrors concepts like Bayesian inference, where conclusions shift as stronger evidence is introduced. Your claim works the same way the more precise your documentation, the stronger your position becomes.

First Steps After a Hail Claim Denial

Take a breath. Then take action.

1. Review the Denial Letter Line by Line

Don’t skim. Analyze.

Look for:

- Specific denial reasons

- References to policy language

- Words like “insufficient” or “inconclusive”

These aren’t dead ends. They’re opportunities.

2. Understand Your Policy

Focus on:

- Deductibles

- Coverage type (ACV vs RCV)

- Exclusions

3. Create a Claim File Immediately

Start compiling:

- Photos and videos

- Inspection reports

- Emails and letters

- Call notes

Organization isn’t optional it’s your advantage.

Re-Inspecting Your Roof the Right Way

This step alone can flip a denied claim.

Why a Second Inspection Changes Everything

Initial inspections are often surface-level.

A second inspection can uncover:

- Hidden shingle bruising

- Granule displacement

- Structural impact damage

What to Look for by Roof Type

Asphalt Shingles

- Circular impact marks

- Granule loss

- Soft bruised areas

Metal Roofs

- Dents

- Fastener damage

- Surface scratches

Tile Roofs

- Cracks

- Chips

- Displacement

DIY vs Professional Inspection

| Factor | DIY | Professional |

| Safety | Risky | Controlled |

| Detail | Limited | Thorough |

| Documentation | Basic | Claim-ready |

| Accuracy | Inconsistent | Reliable |

Strengthening Your Claim with Better Evidence

Evidence wins disputes. Period.

Photo and Video Tips

- Take close-ups and wide shots

- Capture multiple angles

- Document gutters, siding, vents

Use Weather Data

Match your damage to:

- Storm dates

- Hail size

- Wind conditions

Get Expert Reports

Professional reports:

- Identify missed damage

- Provide detailed estimates

- Strengthen your case

This is also where many homeowners realize the importance of understanding ‘How to Document Hail Damage for an Insurance Claim‘, because the difference between weak and strong documentation often determines whether a denial stands or gets overturned.

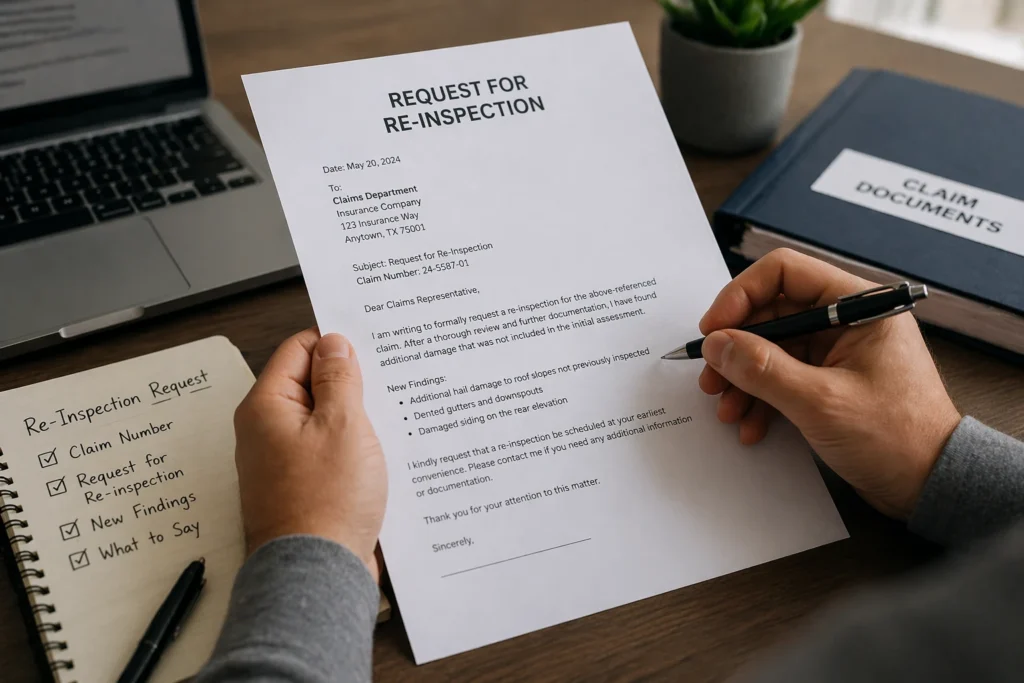

Requesting a Re-Inspection

How to Do It

Put it in writing.

Include:

- Claim number

- Request for re-inspection

- New findings

What to Say

Keep it factual.

Example:

“Additional inspection identified damage not included in the original report. Requesting re-evaluation.”

Have a Professional Present

This increases:

- Accuracy

- Accountability

- Claim scope

Filing a Supplement or Dispute

What Is a Claim Supplement?

A request to include missed damages.

When to File

- After new inspection

- When evidence improves

- When estimates differ

Mistakes to Avoid

- Weak documentation

- Rushed submissions

- Lack of clarity

Case Study: Turning a Denial Into Approval

A homeowner in Irving had a denied claim.

They:

- Got a second inspection

- Documented hidden damage

- Matched storm data

- Requested re-inspection

Result? Full approval.

This happens more often than people realize.

When to Hire a Public Adjuster

What They Do

They:

- Represent you

- Document damage

- Handle negotiations

When You Need One

- Large claims

- Repeated denials

- Low offers

In Irving, where storm claims are frequent, this expertise can make a major difference.

Legal Options If Your Claim Is Still Denied

Appraisal Clause

Independent evaluation process.

Texas Department of Insurance

File complaints if needed.

Legal Action

For serious disputes or bad faith.

Timeline: Why Acting Fast Matters

- Policies have deadlines

- Evidence fades over time

- Delays weaken your case

Act early.

Mistakes to Avoid

- Accepting denial too quickly

- Skipping inspections

- Poor documentation

- Waiting too long

Pro Tips for Success

- Stay organized

- Use professional reports

- Communicate in writing

- Stay persistent

Why Texas Hail Claims Are Unique

- Frequent storms

- High claim volume

- Increased scrutiny

That combination creates more denials but also more reversals.

Conclusion: The Denial Is Just the Beginning

If you’re asking What to Do If Your Hail Claim Was Denied in Texas, here’s the real answer:

You don’t stop.

You build a stronger case.

You challenge the decision.

You push forward.

Because denials are often just the first step not the last.

FAQs

Yes, especially if you have new evidence or request a re-inspection.

It depends on your policy, but acting quickly improves your chances significantly.

Most denials are due to “no storm damage found” or damage being labeled as wear and tear.

Yes, a second inspection often reveals damage that was missed initially.

Yes, but having a professional can strengthen your case and improve results.

Clear photos, detailed inspection reports, and storm data are the most effective.

No, it shows you’re proactive and serious about verifying the damage.

It’s a request to include additional damage that wasn’t covered in the original estimate.

Yes, and this is one of the most common reasons valid claims get denied.

With strong documentation and persistence, many denied claims are successfully overturned.